On 17 June 2025, the European Commission presented a legislative proposal to gradually and effectively end the import of gas and oil from Russia into the EU by the end of 2027.

The planned measures follow the REPowerEU roadmap and provide for the following steps:

- No new import contracts for Russian gas may be concluded from 1 January 2026.

- Cessation of imports based on existing short-term contracts by 17 June 2026.

- Short-term contracts for pipeline gas to be supplied to landlocked countries that are linked to long-term contracts are permitted until the end of 2027.

- Imports under long-term contracts will be discontinued by the end of 2027.

- Long-term contracts for LNG terminal services for customers from Russia or for customers controlled by Russian companies will also be prohibited.

- Oil imports from Russia are also to be phased out by the end of 2027.

The proposal submitted by the EC was based on the assumption that LNG supply (keyword: LNG wave) will increase significantly in 2026 and beyond, and on the timetable that OMV-Petrom will begin the ramp-up phase for production from the Neptun Deep field (Black Sea) from 2027, thus bringing significant quantities of natural gas onto the market.

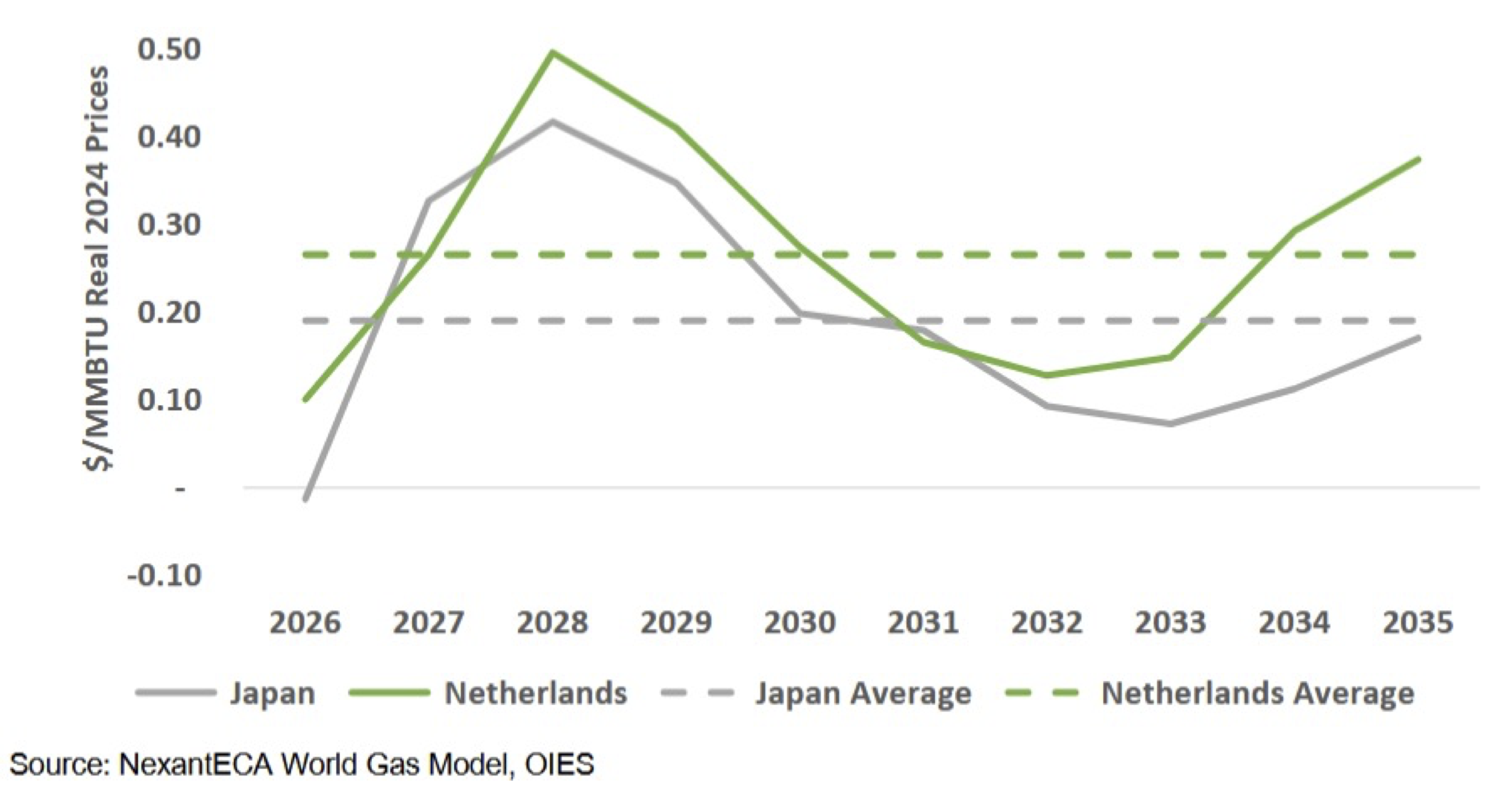

This finely tuned proposal would have led to only minor increases in natural gas prices - including in the landlocked countries of Austria, Slovakia and Hungary. See expected price changes on the TTF and in Japan - shown in the chart below, taken from the Oxford Institute for Energy Studies (OIES). In Austria, the transport-related surcharge must be added to the TTF price.

President Trump has now made further US sanctions against Russia conditional on European partners - including Nato member Turkey - imposing high tariffs on Chinese imports and no longer buying Russian oil.

Following talks with US President Trump today, 17 September 2020, EU Commission President Ursula von der Leyen announced an initiative to stop all European oil and gas imports from Russia more quickly - without giving any further details.

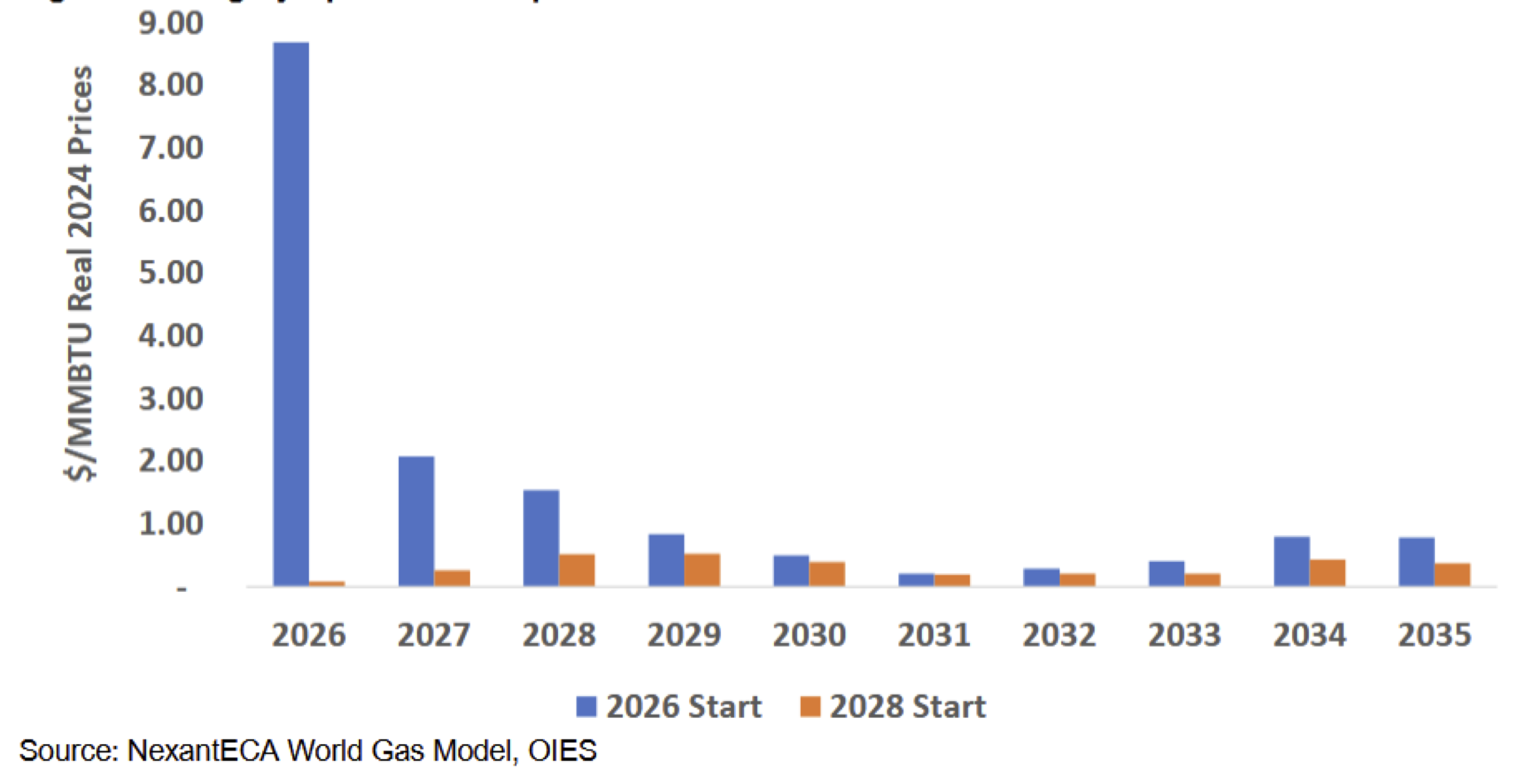

What would an early phase-out of Russian natural gas mean - as indicated by U.S. Energy Secretary Chris Wright in a conversation with EU Commissioner Dan Jorgensen (Wright: "I think this could easily be done within 12 months, maybe within six months)"? Assuming that Russian natural gas can no longer be imported into the EU from the beginning of 2026, this would have the following impact on spot prices

For the TTF price, the price increase compared to the reference price would be significantly higher - precisely because the LNG wave would not yet have (fully) started and Neptun Deep would not yet be producing any natural gas.

In countries such as Hungary and Slovakia, but also in Austria, the price impact would be dramatic - see the following chart - taken from the OIES - which shows the expected spot price increase compared to the reference price in Hungary.

In Austria, Hungary and Slovakia, spot prices would rise to over $20/MMBTU - the TTF spot price would be $11/MMBTU - also with an early exit from Russian natural gas (to arrive at the MWh prices, the price/MMBTU must be multiplied by 2.92). In Austria, you would therefore have to pay around €58/MWh (spot). In Germany, Italy, the Czech Republic, Switzerland and Slovenia, prices would be around $18/MMBTU (= approx. €53/MWh) - in Norway, the Netherlands, the UK, France, Portugal, Greece, Turkey, Bulgaria and Croatia, $11/MMBTU (approx. €32/MWh) would be expected.

It can be seen that in countries that import both pipeline gas and LNG - with the exception of Germany - much lower prices can be expected than in landlocked countries. Since the LNG regasification capacity in Italy is fully booked, no additional LNG can be regasified in Italy - as a result, the prices in Italy - as already mentioned above - will rise to approx. 18$/MMBTU (= approx. 53 €/MWh). As already described in some of the articles published here, Austria cannot hope for high imports via Italy - despite sufficient entry capacity in Arnoldstein.

The later the complete phase-out of Russian natural gas is completed, the lower the increase in natural gas prices in Austria could be.