The latest satellite images show that gas is being flared at the Arctic LNG 2 plant. This could indicate a possible restart of the LNG liquefaction plant - after months of downtime. It is more likely that this is "just" periodic maintenance work. This is because the surrounding water in the loading zone is still frozen - meaning that LNG tankers that are unable to break through the ice, which is sometimes several metres thick, cannot be refuelled. This is against the background that a sufficient number of reinforced LNG tankers are currently not available for Arctic LNG 2.

Nevertheless, the question arises as to whether Arctic LNG 2 could resume operations as early as the summer months of 2025 - against the backdrop of talks between the USA and Russia in connection with a possible ceasefire in the Ukraine war. The export of liquefied natural gas via Arctic LNG 2 must be analysed from different perspectives - last but not least - from the point of view that natural gas from Russia can currently only be transported to Europe via the TurkStream pipeline. All other pipeline routes are blocked either for technical or political reasons - especially as the Sudzha metering station was recently destroyed - meaning that the Ukraine route can no longer be used, at least temporarily, for technical reasons. Even if the relevant pipelines were to be repaired, additional pipeline transport of Russian natural gas to the EU would be very unlikely in the long term because the EU wants to become independent of Russian natural gas. For short-term transports, the lack of progress on ceasefire agreements at least represents a deal-breaker.

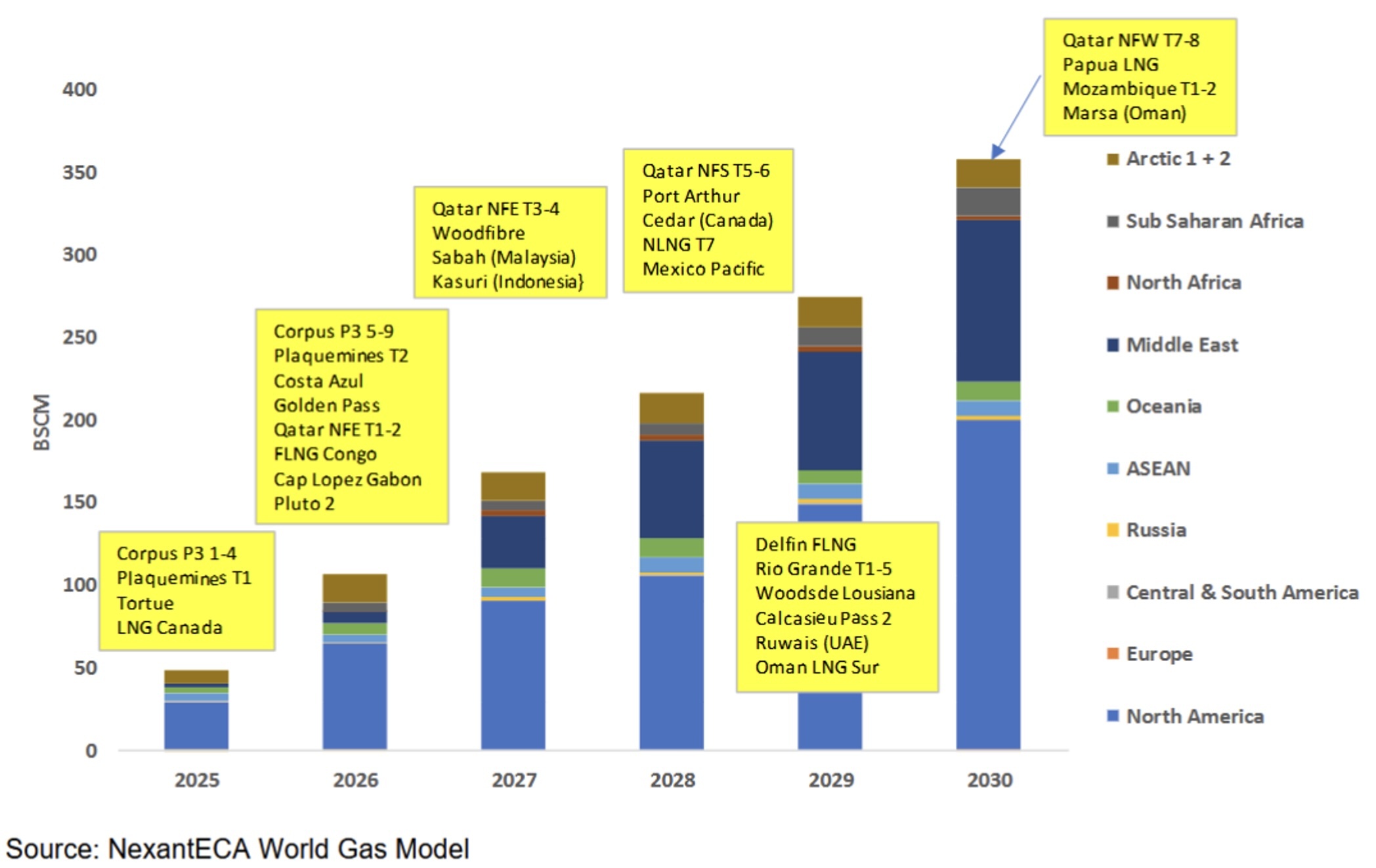

The recent thaw between the US and Russia could lead to the US lifting the sanctions imposed on Arctic LNG 2 some time ago. It appears that even if the intended ceasefire agreement fails, the USA and Russia want to strengthen bilateral relations again, which could greatly reduce Russia's economic isolation. While Russia can market LNG produced in the Sakhalin and Yamal plants outside the EU with almost no restrictions, the EU has sanctioned the transshipment of LNG in the relevant EU ports. If Arctic LNG 2 were to go into operation in the summer months of 2025, this LNG volume would coincide with the additional LNG volumes available in parallel from other liquefaction plants in various countries - so-called "LNG waves". This would result in the additional LNG liquefaction capacity by 2030 shown in the chart below. 340 billion Nm3/year of additional liquefaction capacity is expected to come online by 2030 - without Arctic LNG 2 - i.e. the Arctic LNG 2 volume would account for around 5% of the additional liquefaction capacity available by 2030.

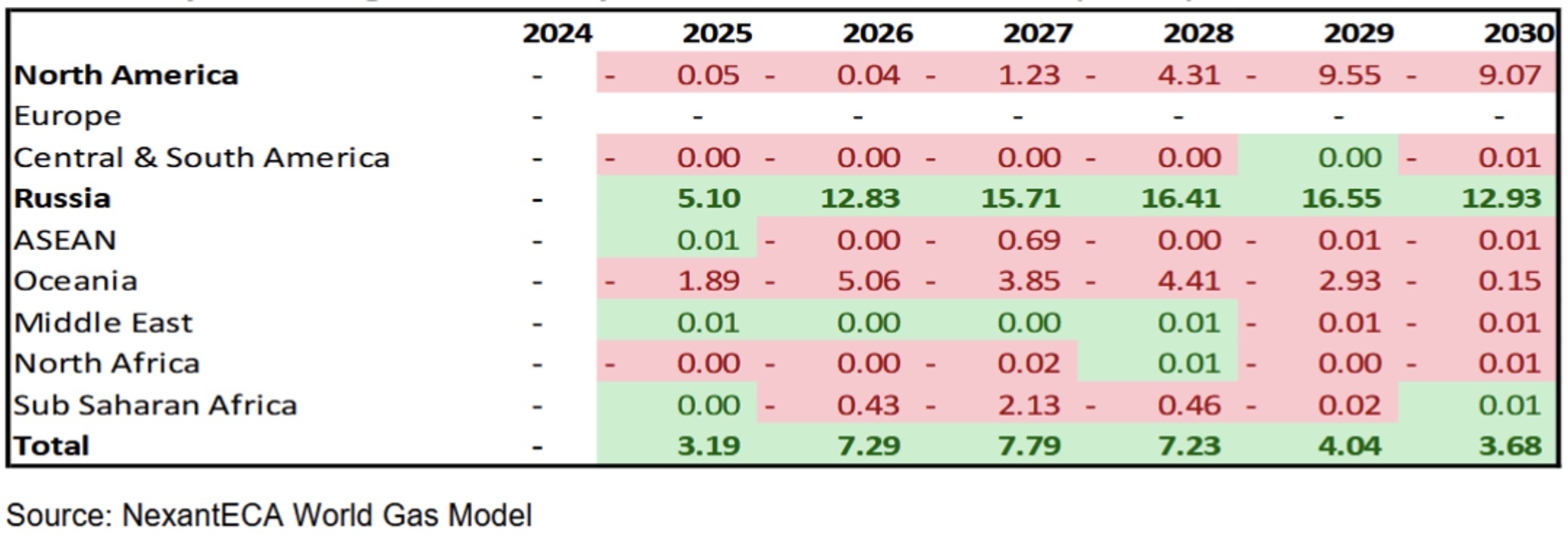

The global distribution of the supply of Arctic LNG2 volumes could look as follows, since the EU does not want to take up any Arctic LNG2 volumes - see chart below.

As already mentioned, the USA would have to lift the secondary sanctions against companies wishing to purchase liquefied natural gas from Arctic LNG 2 - as soon as possible so that LNG deliveries could begin as early as mid-2025, meaning that no icebreaker-capable LNG tankers would be required in Q3 - taking into account the EU sanctions with regard to transshipments in the relevant EU ports.

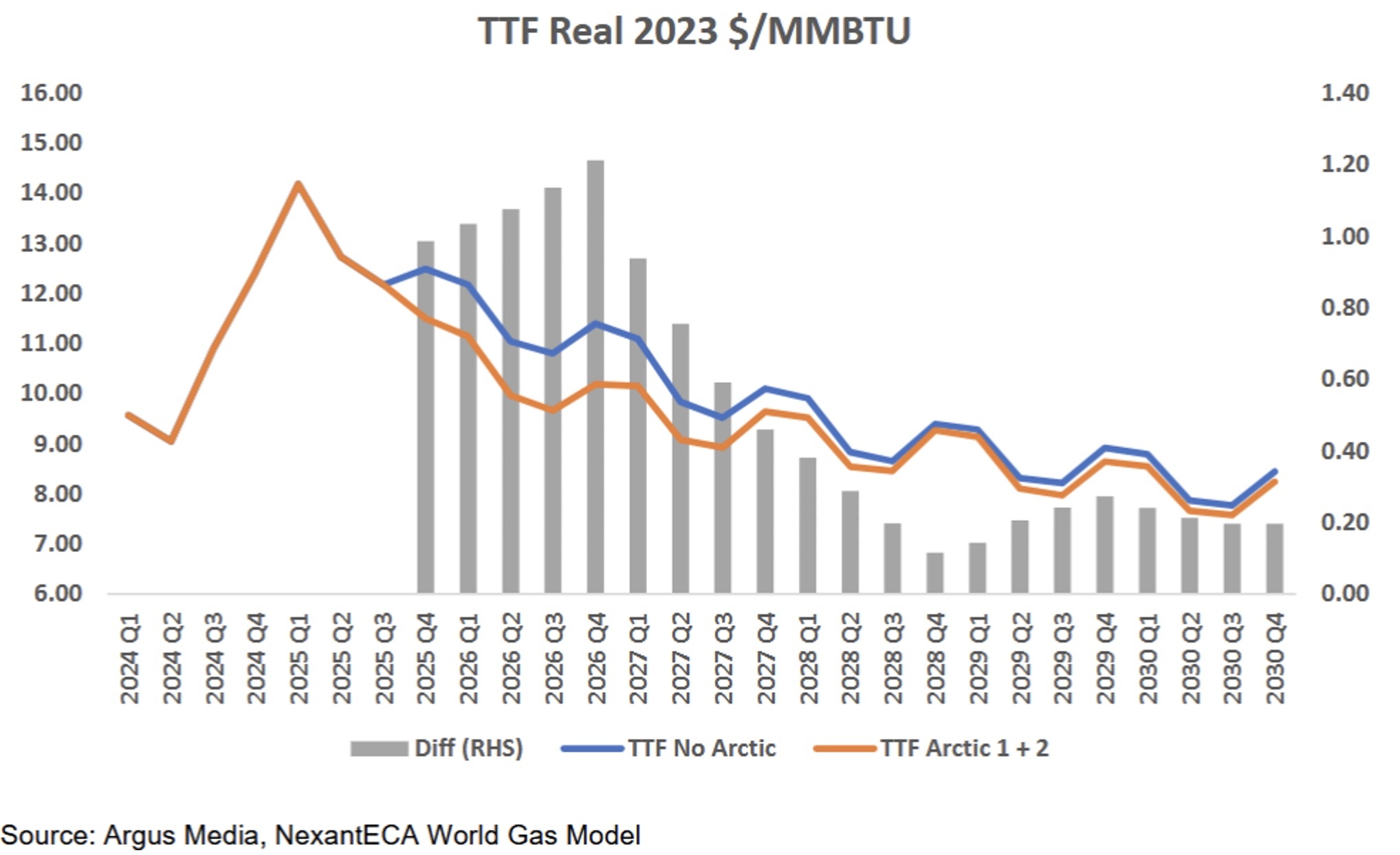

If the scenarios described above materialise, the additional Arctic LNG2 volumes on the world market - even though they would not be purchased in the EU - could reduce the price on the TTF market as shown in the following chart.

It can be seen that the price (basis 2023) in Q4 on the TTF would fall by approx. 3.5 €/MWh (approx. 1 $/MMBTU) due to the "additional volumes" available worldwide caused by the recommissioning of Arctic LNG2. Caused by the "LNG wave" starting in parallel, the price reduction would increase to around €4.2/MWh by Q4 2026 before the price reduction would then decrease and amount to around €1.2/MWh in 2030.

While the sanctions imposed by the West have frozen Russian plans to expand its own LNG sector, the lifting of US sanctions would allow the final investment decision (FID) to be made for additional Russian LNG projects. These plants would go into operation after 2030, meaning that the LNG wave could be extended.